Photo Stephen Li Jen © Eurizon

In a world shaped by intensifying global competition, economic change and technological disruption, where are the investment opportunities in China and Asia?

By Stephen Li Jen, CEO of Eurizon SLJ Capital

Over the past few years, the global backdrop has changed profoundly, marked by a gradual transition from a largely cooperative phase to one increasingly driven by structural competition, particularly between the two major powers, the United States and China. Looking ahead, major global players such as China, the United States, Europe and emerging countries are expected to become increasingly involved in a system shaped by political, economic and technological and innovation-driven rivalry. In this context, emerging markets will also need to adapt to the changes under way and assume a more clearly defined role within global competition, as already demonstrated by South Korea and Taiwan in the technology sector.

In an environment of profound structural change, investors face the challenge of broadening their investment horizons globally, and emerging markets represent an important source of opportunities.

First, the distinction between emerging and developed countries is increasingly fading: economies such as Taiwan and South Korea now post per capita GDP in US dollars comparable to that of Germany or Italy.

More broadly, emerging markets continue to trade at valuations that are significantly more attractive than those of more developed regions. This is also reflected in the positive correlation between expected earnings growth and price-to-earnings ratios (P/E). In principle, sectors or countries with higher earnings growth should command higher valuation multiples. A broader review of the markets represented, however, shows that many emerging countries – such as Taiwan, South Korea and the technology sector in Hong Kong – combine strong earnings growth with valuations that remain undervalued relative to fundamentals.

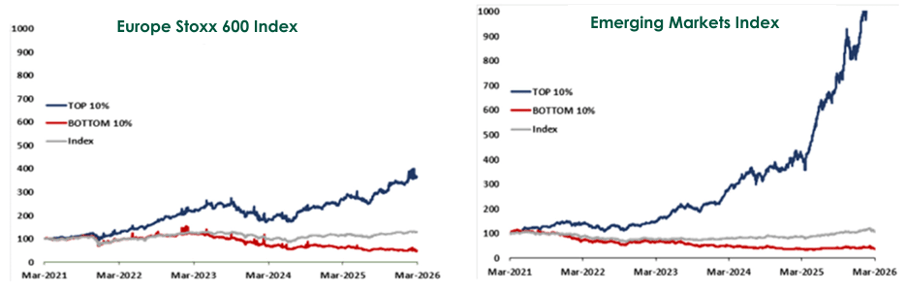

Against this backdrop, a more practical question arises regarding how to access emerging markets. In this respect, it is important to note that traditional emerging market indices were created many years ago and no longer adequately reflect current conditions, as they encompass highly heterogeneous realities and tend not to reward “high-quality investment stories.” The data shown in the charts below indicate that, in emerging markets, the top 10% of companies delivered performance well above that of the overall index; in the European market, by contrast, this gap appears markedly less pronounced.

Source: Eurizon SLJ Capital calculations – March 2026 data

For these reasons, a selective approach focusing on high-quality individual companies to gain exposure to emerging markets appears more advantageous than a broader, more generic allocation to the overall index.

After a difficult period, 2020 marked a turning point for China’s economic policy, with a gradual shift from a model focused on maximising growth to one centred on structural reforms and greater sustainability. One of the key elements of this reform phase has been the reduction in the size of the property sector, aimed at rebalancing the development model and lowering the risk of a bubble burst, similar to the one that hit the Japanese economy in the early 1990s.

China’s economy is now powered by a different engine than in the past, namely technology. In this context, technological and economic competition with the United States is a key lens through which to interpret industrial policy decisions and investment opportunities. China’s strategy can be summed up by the so-called “80/20” approach: achieving a very high level of technological performance (80%) at significantly lower cost (20%). This approach is clearly visible both in the robotics industry and in the artificial intelligence ecosystem, where Chinese solutions are generally competitive not because they hold an absolute technological lead, but because they are highly efficient on a value-for-money basis (DeepSeek).

For investors, this approach implies a different view of global technological competition: it is not simply a battle between winners and losers, but an environment in which operational efficiency and execution speed play an increasingly central role in the dynamics of value creation.

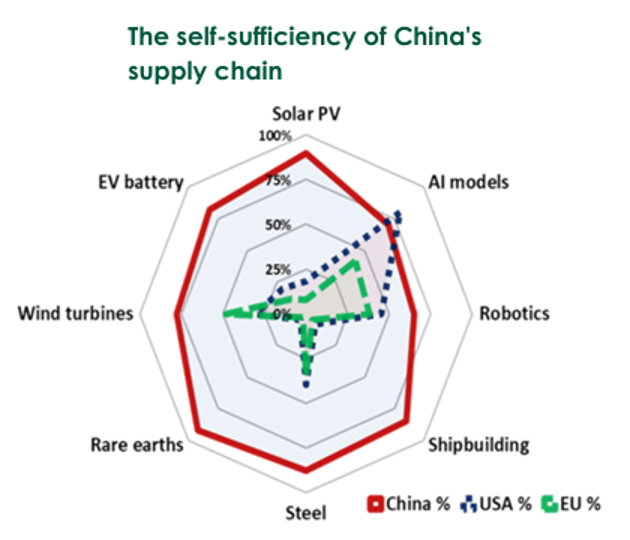

From an equity market perspective, China offers attractive investment opportunities thanks to the specific features of its economic system. One of the main sources of China’s competitive advantage lies in its high efficiency, not only in terms of cost but also operationally. The ability to produce faster and under more favourable economic conditions than other countries offers significant profitability potential, especially for export-oriented companies. In recent years, the export sector has undergone a marked shift, moving from low value-added production to technologically advanced goods such as electric vehicles and solutions for the energy transition. This structural transformation has strengthened the competitive position of many Chinese companies in global markets and made them increasingly interesting for international investors. Another advantage lies in the resilience of the supply chain, which has been developed and reinforced, particularly over the past five to seven years. China has built a holistic, integrated industrial ecosystem spanning a wide range of sectors, from raw materials to artificial intelligence and robotics, including new energy. This structure provides a high degree of flexibility and a better ability to adapt to different market scenarios.

Another structural factor supporting the Chinese equity market is the sheer scale of the economy; in more than 40 industrial sectors, China holds over 50% of global market share. This scale translates into considerable bargaining power in cost management as well as rising pricing power, with positive effects on margins and earnings. In this context, China’s export-oriented sectors represent a highly attractive investment opportunity that can be accessed by selecting companies distinguished by strong “pricing power” in their respective industries. Over the medium and long term, technological- innovation is another fundamental driver of the Chinese equity market. Research and development spending is widespread nationwide and is creating the conditions for new technological revolutions across various sectors, such as electric vehicles, batteries, semiconductors and AI.

Source: Eurizon SLJ Capital calculations – Data as of 9 April 2026

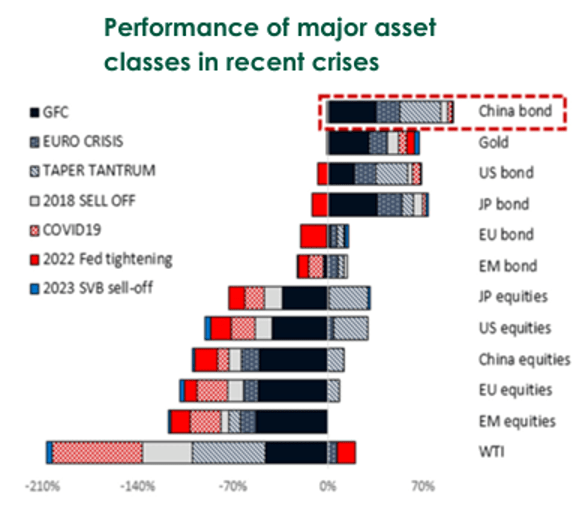

China’s bond market represents a total volume of around $25 trillion. Its main characteristic compared with the bond markets of industrialised countries is low volatility, structurally below 3% in local currency. This profile makes Chinese bonds particularly effective not only within multi-asset portfolios, but also as a core component of fixed-income portfolios, as they contribute significantly to overall stability and to an improved risk/return profile. Moreover, empirical analysis over the past eight years (since the launch of the Eurizon – Bond Aggregate RMB fund) shows that Chinese fixed income securities have displayed particularly strong resilience during periods of risk aversion, establishing themselves as an effective diversification instrument.

From a credit perspective, the environment now appears more favourable than it did recently. Over the past three to four years, China has progressively but decisively restructured the property sector, with defaults concentrated in certain areas. This process is now largely complete: the weakest issuers have left the market, while those remaining have stronger fundamentals. Even in the local government financing vehicle (LGFV) segment, the market is broadly more “balanced” and less vulnerable than other segments of the global credit market. Compared with developed countries, where credit spreads remain tight after years of exceptionally accommodative conditions and concerns over private credit are intensifying, credit risk in China appears relatively limited.

Source: Eurizon SLJ Capital calculations – EUR unhedged performance

Find all our Growth articles