Photos © Muzinich & Co

We believe the ox’s calm and measured character will likely be reflected in China’s economic and political stance in 2021, which could create opportunities for investors

Chinese New Year heralds the Year of the Ox. While the West sees the bull as the symbol of rising markets, in China the ox stands for seriousness and perseverance.

In our view, Chinese policymakers should steer the economy with the ox’s qualities in mind. We may see more measured and targeted structural measures, rather than the rollout of a broad, one-size-fits-all policy.1

Cyclical Recovery

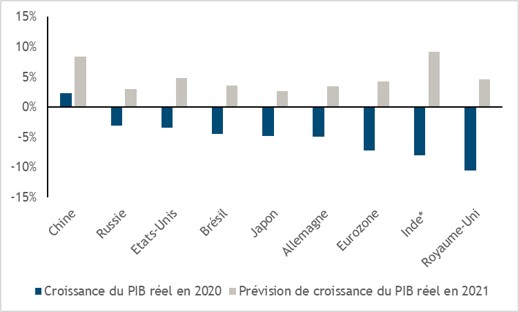

Despite the pandemic, China was the only G-20 country to post positive GDP growth last year: 2.3% in 2020 and 6.5% in the fourth quarter.2

Growth was driven by the containment of the pandemic, a strong rebound in exports (particularly medical and electronic equipment), and government support measures.3 At the start of the pandemic, the People’s Bank of China (PBoC) eased monetary policy. However, unlike other central banks, the PBoC did not resort to quantitative easing or negative rates. Instead, it deployed a range of structural measures.4

For 2021, the International Monetary Fund expects China to grow by more than 8%, prompting some market participants to warn that this “viral expansion” needs to be kept in check.5 This growth rate is not only a return to pre-crisis levels, but also exceeds the medium-term potential of the Chinese economy. Yet, in our view, the PBoC is already showing signs of normalising its monetary support, without making any abrupt adjustment.

Chart 1. China generated positive real GDP growth in 2020

In February, the PBoC confirmed its targeted structural approach. Monetary policy, it said, should be “precise, reasonable and moderate, striking a balance between economic recovery and risk prevention”.6

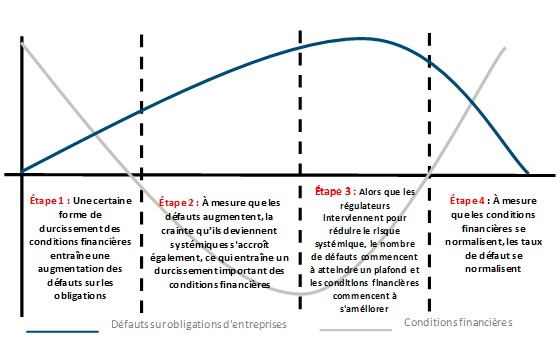

Moreover, we do not view the recent defaults by a few Chinese state-owned entities as the start of a credit crisis. 7

Rather, we believe the economic recovery has brought balance sheet repair back onto the agenda.

In our view, the spillovers from onshore markets to offshore credit markets create an investment opportunity. While we believe the widening of spreads on Chinese high-yield bonds is driven by fears of systemic defaults and a hard landing, the number of defaults should remain low.

As Chart 2 shows, we now appear to be in the fourth stage of the default cycle: the normalisation of financial conditions and default numbers.

Chart 2. The four stages of the default cycle for Chinese onshore corporate bonds

COVID-19

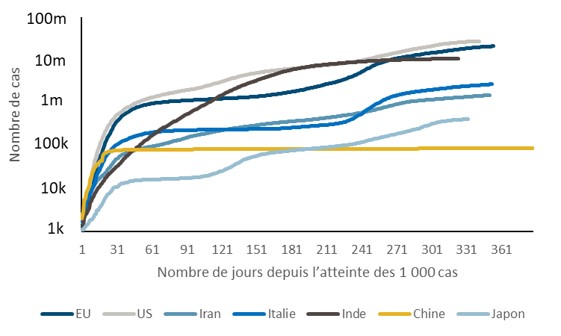

As the whole world was forced to wage a massive battle in 2020 to contain and defeat COVID-19, we believe China’s management of the outbreak was remarkably effective. Targeted measures — draconian lockdowns and digital surveillance systems used to track cases — made it possible to eradicate the virus, and the vaccination campaign is already well underway. 8

So far, China’s economic recovery has been driven by industrial production. In our view, the next phase of the rebound will need to rest on stronger domestic consumption, which in turn will depend on keeping the pandemic under control.

Chart 3. Global COVID-19 cases

Currencies

We believe China’s approach to currency management will resemble that of the measured ox.

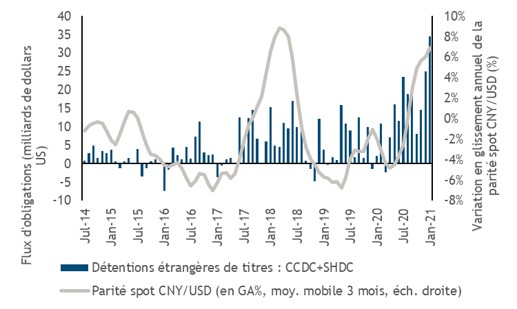

In 2020, the yuan strengthened by nearly 7% against the US dollar, in our view driven by a V-shaped economic recovery, capital inflows and interest-rate differentials.9

In January 2021, the PBoC rebalanced the currency basket within its exchange-rate management system — the China Foreign Exchange Trade System — against which the yuan is managed. It lowered the weighting of the US dollar in favour of the euro.10 This is the second adjustment since the basket was introduced in 2015, and according to the PBoC this move reflects China’s foreign trade conditions.11

One could argue that this decision is a response to the new trade agreement signed with the EU at the end of last year. But we also believe this move reduces China’s overall dependence on the US currency for its trade flows.

In a year of declining foreign direct investment globally, China still attracted $163 billion in 2020.12 Its domestic bond market benefited from record capital inflows as Chinese government bonds were added to major sovereign indices, while Chinese equities gained 26%.13

Even if a further appreciation of the yuan could weaken exports and run counter to the country’s broader policy of boosting domestic consumption, we believe the authorities should not resort to drastic monetary measures.

In our view, a currency war could be too damaging this early in the relationship between China and the new US administration led by Joe Biden. An interest-rate cut could also prove problematic. We believe policymakers are trying to avoid imposing broad measures that typically trigger a generalised expansion. As a result, interest rates and the yuan should, in our view, remain stable.

Against this backdrop of stability, we expect capital inflows to continue in 2021. While foreign positions in Chinese government bonds have risen, they could still increase further, particularly as these securities are gradually added to indices.14

Most flows into the Chinese onshore renminbi (RMB) market have gone into government bonds or bank bonds. In the case of RMB-denominated corporate bonds, the appetite to move down the credit-rating scale remains limited.15

We think this is due to two reasons. First, these securities are mainly purchased by government-bond mandates. Second, we believe credit spreads and rating differentiation among Chinese onshore bond issuers are still too narrow.

Chinese hard-currency bonds appear better suited to corporate-credit investors, given their liquidity, credit-spread differentiation and ratings.

Chart 4. Strong bond inflows have fuelled the RMB’s upward trend

Climate

In 2020, China committed to achieving net-zero carbon emissions by 2060.16 The country is one of the world’s largest carbon emitters, but it is also a major investor in green energy. Its green bond market has therefore expanded from just $1 billion in 2014 to $165 billion at the end of 2020. 17

To meet its net-zero target, the country will need to cut carbon emissions by at least 85% by 2060. 18 It will need to invest RMB 3 to 4 billion ($433 to $577 billion) per year to achieve that goal, and we believe green bonds could be an effective financing tool in that context.19

We could see green bond issuance of nearly $500 billion globally, with Chinese issuers accounting for a substantial share. That would offer investors numerous opportunities in a fast-growing market segment.20

However cynical one may be about China’s carbon-neutrality goals, it is worth noting that the central government has already set annual province-by-province targets for the share of renewables in total electricity consumption through to 2030.21

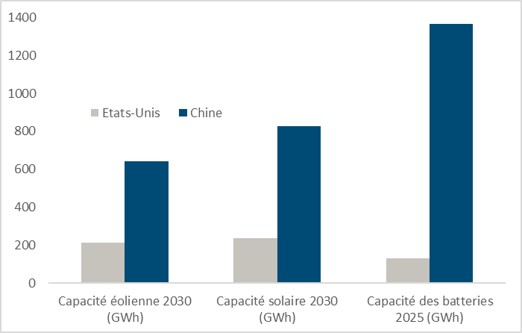

Chart 5. Clean technologies continue to gain ground in China

China–United States relations

It is too early to say whether US-China relations will change in substance or style after President Biden’s election.

Because of the pandemic, China missed its Phase 1 commitments under the trade agreement by 30%. Energy purchases suffered the biggest delays, while commitments to buy US agricultural products were the best observed.22 Since these targets were not met, we believe President Biden could extend the deadline or renegotiate the terms of the deal.

However, we may see ongoing tensions between the two countries. Joe Biden’s climate envoy, John Kerry, has already criticised China’s 2060 net-zero target, which is 10 years later than the other major emitters.23

In our view, the new economic policies set out at the Central Economic Work Conference in December 2020 make it clear that China is trying to turn inward and strengthen its domestic market. To do so, it is seeking to become less dependent on industrial supply chains and external technologies, foreign demand and even the country’s ability to feed itself.24

Policies such as “strengthen China’s ability to control industrial supply chains”, “strengthen national strategic technologies” or “expand domestic demand” all speak to this push for less dependence on the United States and other countries. Even the recent rebalancing of the currency basket against which the yuan is managed reflects this reduced dependence on the US dollar. 25

In our view, trade tensions and US sanctions on Chinese issuers have weighed on the prices of Chinese investment-grade corporate bonds. As a result, we believe these tensions around the status quo are already priced in.

A serious deterioration in China-US relations, such as a hard line from Washington on the Phase 1 trade deal, would, in our view, have a negative impact on markets.

But that is not our central scenario, as Biden is likely to have more pressing domestic issues to address. Nonetheless, none of the geopolitical tensions so far appear to have discouraged investors from putting money into China, which may indicate their underlying confidence in the Middle Kingdom.

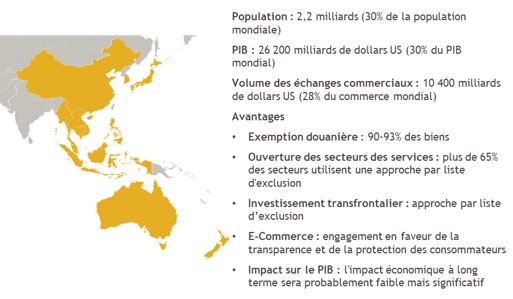

We also believe the relevance of the new trade partnerships signed at the end of last year should not be underestimated, such as China’s new trade agreement with the EU and the Regional Comprehensive Economic Partnership.26

Chart 6. Regional Comprehensive Economic Partnership free trade area

Conclusion

Looking ahead, in this Year of the Ox, we believe playing the reflation theme through China should prove sensible. We think policymakers will take a cautious and measured approach to growth this year, in keeping with the patient ox of Chinese folklore.

In our view, China, like many other countries, should see a year of solid growth while tackling bigger structural issues such as climate change, the consolidation of domestic consumption and the normalisation of financial conditions.

About the author: Christiana Bastin, Portfolio Manager

Christina joined Muzinich in 2013. An experienced portfolio manager, she has built an outstanding 25-year career in corporate bonds. Before Muzinich, Christina held a number of credit and trading roles at Deutsche Bank, including managing bank risk portfolios. Prior to that, she was a credit analyst at Schroders Investment Management and Commerzbank. She also worked at Fitch Ratings (1995-2000), where she was responsible for rating Korean banks during the 1996 Asian crisis and Japanese banks during the country’s banking crisis. She holds a BA from the University of Oxford and an MA from the University of London. She also received a Yamamuro Trust Foundation Scholarship, which enabled her to complete a one-year programme in International Politics at Keio University (Tokyo). Christina speaks five languages fluently.

Footnotes:

Important information

The Muzinich & Co. company mentioned in this document is defined as Muzinich & Co. and its affiliates. This document has been prepared for information purposes only and, as such, the views expressed herein should not be regarded as investment advice. The opinions expressed are valid as of the publication date and are subject to change without notice or reference. Past performance is no guarantee of future results. The value of investments and the income from them may go down as well as up and are not guaranteed, and investors may not get back the amount originally invested. Exchange rate movements may cause the value of an investment to rise or fall. This document, together with the views and opinions it contains, should under no circumstances be construed as an offer to buy or sell any investment product or as an inducement to invest, and is provided for information purposes only. The opinions and statements regarding financial market trends, based on prevailing market conditions, reflect our judgment as of the date of this document. They are believed to be accurate at the time of writing, but Muzinich cannot guarantee their accuracy and accepts no liability for any error or omission. Some of the information in this document constitutes forward-looking statements; due to various risks and uncertainties, actual events may differ materially from those reflected or contemplated in these forward-looking statements. Nothing in this document should be regarded as a guarantee, promise, assurance or claim regarding the future. All information contained in this document is believed to be accurate as of the date indicated, is not complete and may be changed at any time. Some information contained in this document is based on data obtained from third parties and, although believed to be reliable, has not been independently verified by Muzinich & Co. or any Muzinich & Co. affiliate, and its accuracy or completeness cannot be guaranteed. Risk management involves an effort to monitor and manage risk, but does not imply low or no risk. Emerging markets may be riskier than more developed markets for a variety of reasons, including but not limited to heightened political, social and economic instability, greater price volatility and lower market liquidity. In Europe, this document is published by Muzinich & Co. Limited, authorised and regulated by the Financial Conduct Authority. Registered in England and Wales under number 3852444 Registered office: 8 Hanover Street, London W1S 1YQ, United Kingdom. Muzinich & Co. Limited is a subsidiary of Muzinich & Co, Inc. Muzinich & Co., Inc. is an investment adviser registered with the Securities and Exchange Commission. The fact that Muzinich & Co, Inc. is a registered investment adviser with the SEC does not in any way imply a certain level of skill or training, nor any authorisation or approval by the SEC.

Market index descriptions

It is not possible to invest directly in an index, which also does not take into account commissions or trading costs. Index volatility may differ materially from the volatility of the performance of an account or a fund.

Shanghai Shenzhen CSI 300 Index – The CSI 300 is a float-adjusted market-capitalisation-weighted index comprising 300 A shares listed on the Shanghai or Shenzhen stock exchanges. The index’s base level is 1,000 as of 31/12/2004